At the 2019 AAO annual meeting, AAO Chief Executive Officer David Parke, MD, called it the “most disruptive force in ophthalmology today.” He was describing the rise of the private equity (PE) firm as a new buyer of medical practices.

What it means long-term remains to be seen. For now, however, every ophthalmology practice needs to be aware of its presence as well as the potential benefits and pitfalls.

In a nutshell, PE represents a new type of buyer for the MD owner or group looking to sell their practice. They are one of four options available today. Each is listed below with a specific comment:

- Sell to associate. This is getting harder to do, given medical school debt loads and shifts in work/life prioritization. Average buyout is $500K. This option is near impossible for a large practice with one owner (eg, > $10 million annual collections).

- Sell to hospital/health-care system. Eye surgery is not very attractive to hospitals or systems in large part due to recent innovations that allow ophthalmic surgery to be performed in an ASC or – pay attention to this – in the office. Similarly, being employed by a health-care system doesn’t appeal to the independent spirit that characterizes ophthalmologists.

- Consolidate with a local practice. Joining forces with a local “competitor” is an immediate transaction payout and will be worth more than selling to an associate.

- Partner with a PE firm. Financial payout two- to four-times more than other options.

That multiplier alone makes PE difficult for a doctor to ignore when considering options for the future and eventual retirement. First, let’s explore why ophthalmology is attractive to PE and why now.

About these PE firms

PE’s goal is to find a business that they can buy and control. They want to improve the financial profitability of the enterprise over a five- to 10-year period so they can then turn around and sell it to another buyer, generating a sufficient return to their investors. Unlike public equity markets, PE transactions are not reported or disclosed to the public, making it more difficult to evaluate whether they are successful.

Health care in general, and medical practices specifically, have become increasingly attractive investments. Dermatology and dentistry provide strong precedents for ophthalmology; PE consolidation has taken place in those specialties for 10 to 20 years. Ophthalmology has high demand (five times the rate of population growth as the population ages) in addition to strong reimbursement, with revenue that can be enhanced via elective procedures (e.g., LASIK, refractive IOLs and dry eye treatments) and retail (ie, optical). As an industry, PE views ophthalmology as “inefficient” in terms of service delivery. It is highly fragmented with thousands of “mom and pop” locations that duplicate effort, especially in back-end operations. A large bubble of owners is moving towards retirement with a shortage of younger MDs to replace them.

In short, PE firms see an opportunity to consolidate by purchasing, investing and then selling down the road at a profit.

An active marketplace of buyers and sellers has emerged over the past three to four years. Low interest rates have made the cost of borrowing inexpensive. Public markets are at an all-time high, and money is shifting away from public markets to private investments. With a huge amount of capital to deploy, an estimated 30 firms (at last count, based on informal research) have invested in ophthalmology through acquisitions among the largest practices in the country. The practices purchased directly by PE firms are called “platforms,” as they typically have in place the infrastructure for future additional “tuck-in” or “bolt-on” acquisitions that can be used to grow that platform. This consolidation under a single owner allows changes to be made in systems, policies and procedures, with the goal of greater efficiency.

Estimates by industry analysts, including BSM Consulting and J. Pinto & Associates, indicate that perhaps 2% of practices and 5% of ophthalmologists have a capital partner in PE to set up for future growth. For perspective, we estimate that at most 20% of dermatology practices have been consolidated over the past 10 to 12 years, with many of those first acquisitions now turned over to new buyers in what is called the “second bite at the apple” for the original doctor owner.

The questions around selling to PE (which is better described as partnering, given that most firms will require the MD owners to stick around for a minimum of three to five years) boil down to “if” and “when.” Let’s look at these one at a time.

If: should we sell?

While a young associate buying into a practice will want to incorporate changes and bring in modern ideas, a PE capital partner will make changes and be in a position of control. This change of control makes a potential sale a hugely emotional decision that does not show up on the spreadsheets or in your bank account. It is the first topic covered when we consult with physicians on the topic of PE.

Given all the unknowns around reimbursement, payers and the overall economy, it can be an equally huge relief to have the burden of practice management put on someone else’s shoulders. That’s what you get when you sell and go from being an individual to part of a team.

For those practices that want to grow as part of long-term consolidation in the specialty, capital partners can help get this done faster than what you can do on your own. They have the money as well as expertise in how to evaluate transactions.

What PE firms do not possess is deep expertise in ophthalmology. We are already seeing challenges posed by smart executives who don’t understand how to effectively run an ophthalmic practice. My prediction is that this will hamper growth in the near term. However, PE buyers are already much smarter than they were several years ago. Evidence can be seen in the shift in the buyer-seller dynamic, which I will describe later in this article.

Colleague John Pinto predicts that independent “boutique” practices will survive without having to sell. . The end of the solo practice has been predicted for a generation. The reality is that because demand for eye care by patients exceeds supply of available providers (MD and OD), patient access will continue to be preserved for the foreseeable future. The “sweet-spot” is three to five doctors in a single location with an ASC and an optical; the farther away from a major metro area, the better.

I agree with John’s assessment, with one key addition — the rise of another PE, “patient experience.” This area will do more to build practice value than any technology or specific procedure. Customer experience, which has firmly implanted itself across virtually every industry, is now making its way into health care. The boutique medical practice that seeks to build its market presence will benefit by becoming increasingly customer-focused and continuously improving its patient experience. The same could be said for the PE-owned practice. Like running any enterprise, though, this becomes harder to do as the organization increases in size (doctors, locations, staff, etc).

When: what is the best time to sell?

While many doctors become fixated on the potential payout from a transaction, they often fail to appreciate how difficult it is to get a deal done. For the professionals involved, this is a transaction that requires immense amounts of financial, legal and regulatory due diligence. It will take anywhere from three to 12 months (or longer) depending on the size and scope of the deal.

The private, undisclosed nature of transactions and negotiations makes it hard to verify the “whisper” numbers that get passed around. When you hear that a practice sold for 10 or 12 times its earnings, take that information with a large grain of salt. The calculation of practice value is subject to numerous adjustments to profitability, which is defined as “earnings before interest, taxes, depreciation and amortization,” or EBITDA. The more accurate normalized EBITDA takes into account the requirements of the professional PE buyer, which are far more and complex than what is needed to sell to an associate or merge with a local practice.

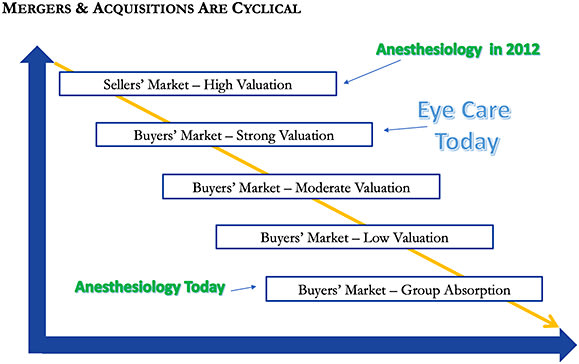

There are signs that the market has already shifted from favoring the seller to the buyer. My sources indicate that the market is active and healthy for ophthalmic practices, but the buyers are much smarter than even two years ago (as noted earlier). This means that there are fewer bidding wars with multiple offers and that transactions are taking longer to complete as buyers’ improved knowledge of ophthalmic practices leads to deeper questions and analysis. What this means for doctor-owners is that, while practice value doesn’t fluctuate based on supply/demand dynamics, the multiple paid does. What may have sold for eight times normalized EBITDA a year ago may now only command six times. This is one market dynamic you do not control. (See Figure, below)

What you do control is what happens in your practice on a daily basis. Regardless of whether you want to sell to PE, you should look for ways to improve the value of the practice. Sometimes this means adding providers or a new location. While our firm advises on these matters, we increasingly see opportunities to unlock “hidden” value in the practice by analyzing current operational and marketing efforts. Additional revenue and bottom-line margin can be found in most practices we have worked with, giving you an opportunity to increase the overall value of the practice without additional investment in staff or equipment.

PE checklist

The following are seven key considerations you need to analyze prior to moving forward with a PE acquisition (in order):

- Motivation: What’s the goal in selling?

- Control: Can you emotionally handle having less control?

- Expertise: Are you willing to recognize and hire resources to help?

- Younger physicians: Can you achieve alignment across generations?

- Practice health: Is your practice ready financially and culturally?

- Market dynamics: Will your practice be attractive to buyers?

- Tax efficiency: Have you fully explored how to optimize and reduce tax exposure?

Summary

The presence of PE and willingness to pay far more for your practice than what was historically available means that you need to pay attention. “To sell or not to sell?” is a fundamental question that only the doctor-owner can answer — preferably after seeking outside help to evaluate options for the future of the practice. In the near term, it helps to think like the PE buyer and ask, “What is our practice worth, and how do we make it more valuable?” In some cases, selling now makes sense and the timing (for now) is good. In other cases, taking the next several years to “renovate the house” is a better path before selling, whether to PE or via merging with another practice.

To the extent the PE capital partner creates additional value by improving the practices they acquire, PE will become increasingly attractive as an option for practices. If their impact falls short of that, then PE is just a bigger version of the “house flipping” seen in residential real estate where they want to buy low and sell high based on market momentum rather than actual value creation.

PE will be with us for a long time — whether its model is sustainable remains to be seen. I expect the model and approach will continue to evolve as both buyers and sellers become increasingly familiar with one another’s needs, as well as how “practice growth” is planned and executed. OM

About the author: