Numbers for Managers: The Balance Sheet

A Snapshot of Your ASC’s Financial Health

By Maureen Waddle, MBA

|

Note: This is the second article in a two-part series designed to help managers better understand the financial statements of their ASCs. The first article, which appeared in February’s issue of The Ophthalmic ASC, focused on income statements. |

Many ASC nurse directors are thrust into management roles without the benefit of any training in financial reporting. After viewing financial data, it’s not uncommon for those new to these positions to voice sentiments of concern similar to those expressed by the nursing director in the following case study excerpt:

“I’m completely lost,” says the nursing director on the other end of the telephone. “This ASC has been operating for more than a year and since I took over a few months ago, our profit and loss statement shows positive income, but there is no money in our bank account. What am I doing wrong?”

In order to make decisions based on good information, the manager must understand and be able to answer questions about information found on the balance sheet.

This nursing director is eventually relieved to learn that she’s not doing anything wrong. She’s just inexperienced at reading and understanding ALL of the organization’s financial statements. Her ASC is in a common financial position faced by many young and growing ASCs. In order to understand her concern and see how easily an individual can be misled by not utilizing all available financial information, it’s necessary to learn the primary functions and limitations of all financial statements. It’s rarely possible to get an accurate and complete assessment of an organization’s financial well being from just one source. Understanding this fact will help directors gain a more thorough understanding of how to interpret important financial data, which in turn will help them make better management decisions.

The financial statement that would have helped this director better understand her ASC’s predicament is the balance sheet. Before we get back to the bewildered nurse director in the case study, let’s examine some basic information about balance sheets.

What is a Balance Sheet?

A balance sheet is a financial report generally prepared by an outside accountant. QuickBooks®, the most commonly used accounting software for small businesses, has standard financial reports set up for balance sheet statements as well as for income statements (profit and loss statements or P&Ls).

For a balance sheet to be of optimal use to an ASC, it must be set up in the organization’s accounting software with appropriate categories. This allows statements to be accurately generated. Of maximum importance, though, is understanding how to use a balance sheet as part of a regular financial review so the report can be optimized as a tool in the ASC’s management decision-making process. Additionally, managers and owners must understand that balance sheets aren’t used solely for their own understanding of the financial health of their ASC, other entities may view these financial statements as well.

The balance sheet is appropriately named because the categories must always be in balance. At any given point in time, the value of what an ASC (or any business) owns (assets) must be in balance with what it owes to creditors (liabilities) or owners (equity). By looking at a company’s assets in comparison to its liabilities and owner’s equity, you can determine the financial position or “health” of the company at a given time point.

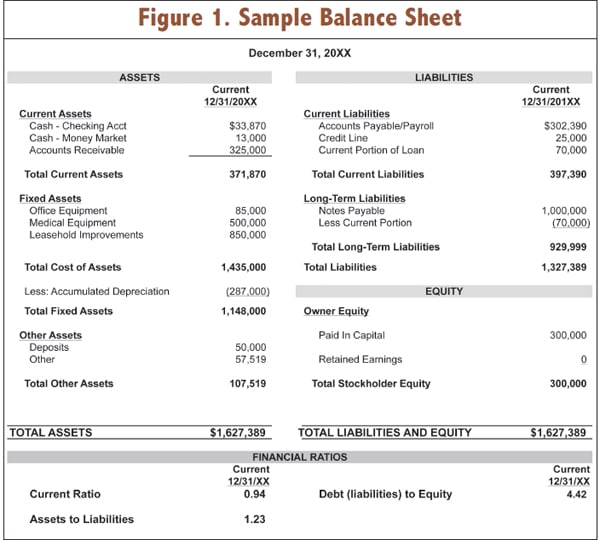

In a typical balance sheet format, the assets are listed on the left side of the sheet, and the liabilities and equity are listed on the right side. The accompanying sidebar (Balance Sheet Terminology) provides definitions of key balance sheet terminology, and Figure 1 shows an example of a balance sheet.

Who Looks at an ASC’s Balance Sheet?

Considering that a balance sheet provides a “snapshot” of the financial health of a company, you can begin to guess who might want to look at an ASC’s balance sheet.

Creditors, for one, may need to view a surgery center’s balance statement. Creditors may include banks or equipment-lease companies that might need to make a judgment about whether or not they should extend credit to the organization. They would make this determination by evaluating assets in comparison to liabilities (see ratio explanations in the accompanying table).

Potential investors or partners may also view the ASC’s balance sheet. They would use a balance sheet, in conjunction with other information, to be confident that they’re buying into a financially viable organization. If the balance sheet shows the business is “highly leveraged” (i.e., it has too much debt) the value to “buy in” would most likely be reduced.

| Common Balance Sheet Ratios | ||

|---|---|---|

|

Ratio |

Formula |

What You Learn |

|

Current ratio |

Current assets divided by current liabilities |

On it’s most basic level, this ratio can answer the question: Can the company meet it’s obligations? A ratio of 1 (or a 1:1) means there is NO working capital. You would like to see this number at least at 2 (meaning the business has twice as many current assets as obligations); but preferably it should be somewhere between 2-6. If the number is much higher than 6, the company should probably look at investments for its excess capital (or pay out dividends to the owners). |

|

Assets to liabilities |

Total assets divided by total liabilities |

This gives you a long-term picture of the company. Again, you’re looking at the ability to meet obligations. The higher the number, the better the general health. |

|

Debt (liabilities) to equity |

Total liabilities divided by owners (stockholders) equity |

This indicates the risk of the company to creditors. The higher this number (indicating significant debt) the more the company is considered to be “at risk.” |

Manager Uses for a Balance Sheet

A business manager (regardless of the official job title) has the responsibility to make business decisions that will maximize the owner’s return on investment. In order to make decisions based on good information, the manager must understand and be able to answer questions about information found on the balance sheet.

Now that you know the people most likely to review a balance sheet and have a basic understanding of definitions for terms related to the balance sheet, take a look at the accompanying sample of a balance sheet. Keeping in mind that the balance sheet reports on the financial health of an ASC business, answer the following question: Is the company represented by the sample balance sheet financially sound?

Having a general understanding of assets and liabilities, you intuitively know that you want the assets to be (much) greater than the liabilities. Beyond intuition, there are some common ratios and benchmarks to help you define this.

Based on this sample balance sheet, at this point in time, it’s fair to assess that this business might need a prescription (but probably not a major intervention) to nurture it back to health. If we turn back to our case study and information beyond the balance sheet, we may start to feel more positive about the business.

Back to the Case Study

Getting back to the nurse director’s concern in the aforementioned case study, we can now address her question about having a positive net income yet no money in the bank. A start-up ASC typically uses significant financing through small business loans (in addition to owners’ paid-in capital) to start the business. By the time this nursing director had joined the ASC, it was operating profitably based on her monitoring the P&L statement. However, she wasn’t monitoring her balance sheet, and therefore only had a cursory understanding of the liabilities. Because principle payments aren’t recorded on a profit and loss statement, she didn’t have the capability to see the debt being reduced (as well as the cash being reduced). These would show up on the balance sheet. The owners, in this particular case, had made a decision to make some extra principle payments to shorten the loan period resulting in a depleted cash flow—despite the positive net income on the P&L. Cash flow statements are a good idea in general, but are especially important for ASCs that are trying to manage loan payoffs. With all three statements (P&L, balance sheet and cash flow) being closely monitored, perhaps the managers and owners might have decided to reduce one of the advanced principle payments or change the timing of a payment.

| Balance Sheet Terminology |

|---|

|

The following list includes basic terminology commonly associated with a balance sheet. |

|

Assets: Resources owned by the ASC |

|

Current Assets — Cash, investments, or other assets that can be expected to convert into cash within the current period (usually defined as “within 12 months from the date of the balance sheet period”). Some examples of non-cash assets might include accounts receivable (money owed to an ASC for services provided prior to the date of the reporting period); notes receivable (money owed to an ASC for loans given, perhaps to an owner or an employee); and inventory of items to be sold in the future (e.g., IOLs). Non-Current Assets — Also known as long-term assets, this includes items that will not be turned into cash or “consumed” within 1 year of the balance sheet. Examples include intangible assets, equipment, tenant improvements and investments. Tangible Assets — Items owned by the company. Tangible assets usually include equipment, furniture, and fixtures, and leasehold improvements. These items are typically valued at the cost of purchase less accumulated depreciation. Intangible Assets — ASCs typically don’t have many intangible assets listed on their balance sheet. Examples of intangible assets include items for which values are difficult to quantify, such as trademarks and patents. Goodwill [not clear on what she means by ‘goodwill’ here] is also an example of an intangible asset that is more commonly seen on a practice balance sheet but certainly may be found on an ASC balance sheet if the company has purchased another ASC or related company. These assets are reported at cost on the balance sheet, though they may have far greater value. |

|

Liabilities: Obligations due to creditors |

|

Current Liabilities — Liabilities that will come due in the current period (same period as current assets). Examples of current liabilities include accounts payable, notes payable, and accrued expenses. Note that liabilities often include the term “payable” in their titles. Long-term Liabilities — All other liabilities not captured in current liabilities. This usually includes bank loans and capitalized equipment leases (less amount paid in current period). |

|

Equity: Company’s obligation to the owners/stockholders |

|

Stockholders’ Equity — If it’s a corporation, the equity is classified as stockholders’ equity. Owner Equity — All other equity types (e.g., sole proprietor, partnerships, etc.) are classified as owner equity. Paid-in-Capital — Also called “contributed” capital, this is the money an ASC or other business has received via an investment from owners or stockholders. Retained Earnings — The profits (revenues less expenses) a business keeps (instead of disbursing the funds to its owners) to cover future business activities. A simpler definition is: The total of all accumulated earnings after taxes and paid-out dividends. This is tracked in the retained earnings accounting item under “equity.” |

Better Understanding

Going through this exercise should help ASC managers gain a better understanding of balance sheets and the players who may have a stake in viewing them. Furthermore, it underscores the importance of being familiar with ALL financial statements. With this knowledge, it’s possible to view an accurate snapshot of the financial health of your ASC so you can make the best data-based management decisions for the organization. ◊

Maureen Waddle, MBA, is a senior consultant with BSM Consulting, an internationally recognized health care consulting firm.